Top Ag News Stories

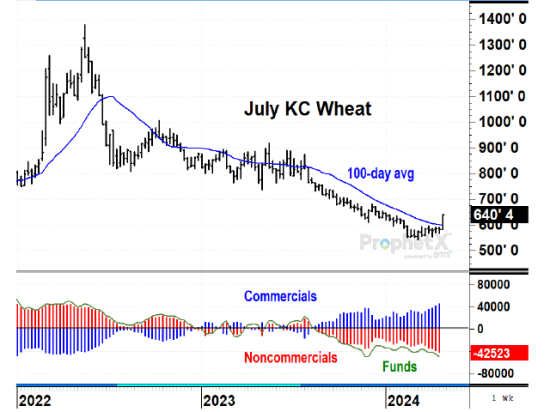

Todd's Take

4/26/2024 | 6:28 AM CDT

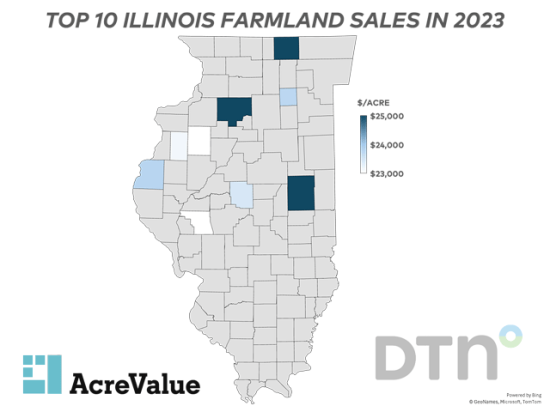

Top 10 Illinois Farmland Sales in 2023

4/25/2024 | 11:40 AM CDT

Taxlink

4/26/2024 | 4:55 AM CDT

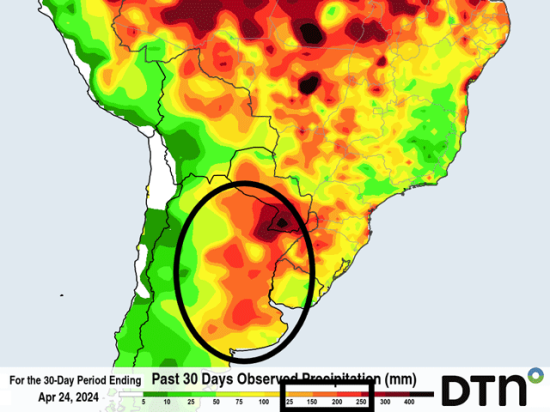

South America Calling

4/25/2024 | 4:27 PM CDT

Call the Market

4/24/2024 | 9:30 AM CDT

DTN Market Headlines

-

USDA Weekly Crop Progress Report

USDA Crop Progress: Winter Wheat Condition Holds Steady at 56% Good to Excellent

-

Cash Market Moves

Panama Canal Increasing Booking Slots Beginning Mid-May 2024

-

Technically Speaking Blog

November Soybean Prices Offer a Spring Riddle

-

Data, Markets and NASS Reports

Producers, Others Raise Concerns Over NASS Dropping Midyear Cattle Report

More Recommended for You

Ag Futures

DTN Featured Blogs & Columns

Sponsored Spotlights

DIM[0x0] LBL[] SEL[] IDX[] TMPL[] T[]

DIM[0x0] LBL[] SEL[] IDX[] TMPL[] T[]

DIM[1x3] LBL[home-page-native] SEL[] IDX[] TMPL[standalone] T[]

5-Day Weather

Outlook

Want to save your postal code for future use?

DTN 360 Poll

The DTN 360 Poll is not available at this time.

DIM[1x3] LBL[home-page-native 2] SEL[] IDX[] TMPL[standalone] T[]